Dog bite incidents create complex legal and insurance challenges for victims, dog owners, and property owners across Missouri and Kansas. Understanding how homeowner’s insurance responds to dog bite claims and when landlords face liability helps families navigate the aftermath of these traumatic events and pursue fair compensation.

Missouri imposes strict liability for dog bites in many situations, while Kansas generally uses negligence/”one-bite” rules; insurance coverage then varies significantly by policy terms, breed restrictions, and prior incidents. Property owners may also face liability when dogs on their premises injure visitors or tenants under specific circumstances.

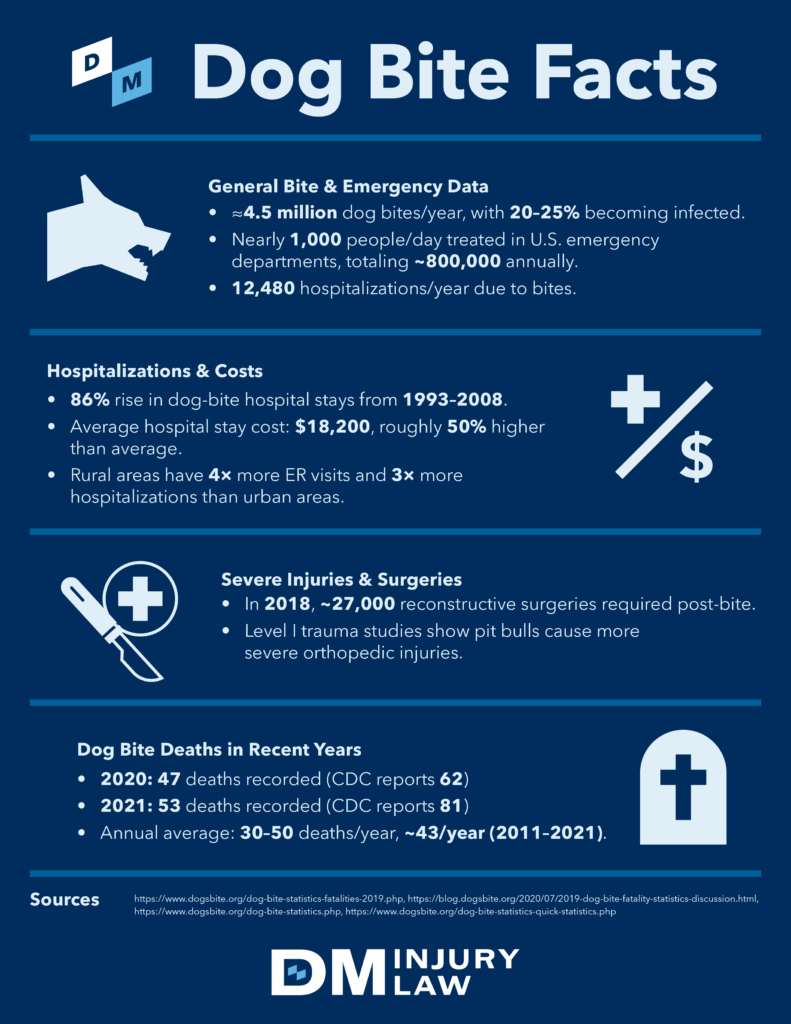

Key Takeaways for Dog Bite Liability in MO and KS

- Homeowner’s insurance often covers dog-bite claims but may exclude certain breeds or limit coverage, depending on the policy and carrier.

- Missouri imposes strict liability for dog bites when the victim is on public property or lawfully on private property; damages are reduced by any victim fault. Kansas generally uses negligence/”one-bite” rules (no statewide strict-liability statute).

- Comparative fault applies: Missouri’s statute allows reduction for victim fault; Kansas follows modified comparative fault (recovery barred at 50%+ fault).

- Insurance companies often investigate dog bite claims extensively and may deny coverage based on policy exclusions.

- Experienced dog bite attorneys help victims navigate insurance disputes and identify all potential sources of compensation.

Table of Contents:

Homeowner’s Insurance Coverage for Dog Bites

Homeowner’s insurance policies generally provide liability coverage for dog bite incidents that occur on the insured property or involve the policyholder’s dog elsewhere. However, coverage varies significantly based on specific policy language, breed restrictions, and the insurance company’s underwriting guidelines.

Most standard homeowner’s policies include personal liability coverage that applies to dog bite injuries caused by household pets. This coverage typically includes medical expenses, legal defense costs, and damages awarded to bite victims up to the policy limits.

Standard Coverage Components

Homeowner’s insurance dog bite coverage typically includes several components that protect the dog owner and provide compensation for victims. Medical payments coverage provides immediate payment for the victim’s medical expenses regardless of fault, usually with lower limits ranging from $1,000 to $5,000.

Personal liability coverage represents the primary source of compensation for dog bite victims and covers damages awarded in lawsuits or settlements. Standard policies often provide $100,000 to $300,000 in liability coverage, though higher limits are available.

Most homeowner’s insurance policies provide coverage for dog bite incidents through several key provisions:

- Medical payments coverage for immediate victim medical expenses

- Personal liability coverage for damages and settlements up to policy limits

- Legal defense coverage for attorney fees and litigation costs

- Coverage extension for incidents occurring away from the insured property

Some policies also include coverage for property damage caused by pets, though this typically applies to third-party property rather than the policyholder’s belongings.

Related: What is the Average Dog Bite Injury Settlement?

Breed Restrictions and Exclusions

Many insurance companies impose breed-specific restrictions or exclusions that limit or eliminate coverage for certain types of dogs. These restrictions typically target breeds perceived as having higher bite risks, including pit bulls, Rottweilers, German Shepherds, and Doberman Pinschers.

The Insurance Information Institute reports that dog bite claims represent a significant portion of homeowner’s liability claims, leading many insurers to implement restrictive underwriting guidelines.

Mixed-breed dogs with characteristics of restricted breeds may also face coverage limitations, even when the exact breed composition is unclear. Some insurers require veterinary breed assessments or DNA testing to determine coverage eligibility.

Prior Bite History Impact

Dogs with previous bite incidents face significant challenges in obtaining and maintaining homeowner’s insurance coverage. Insurance companies view prior bites as strong predictors of future incidents and may exclude coverage or cancel policies entirely.

Some insurers provide one-bite forgiveness but exclude coverage after a second incident. Policy renewals become particularly challenging after dog bite claims, as insurance companies reassess risk profiles and may decline to renew coverage.

Insurance Claim Process and Challenges

Dog bite insurance claims involve complex investigation and negotiation processes that can significantly impact compensation outcomes. Insurance companies typically conduct thorough investigations to determine coverage applicability and assess liability before making settlement offers.

Related: How Long Does It Take to Settle a Dog Bite Claim?

Initial Claim Investigation

Insurance adjusters investigate dog bite claims by gathering evidence about the incident circumstances, victim injuries, and policy coverage terms. They typically request police reports, medical records, witness statements, and photographs of injuries and the incident scene.

Adjusters also investigate the dog’s history, including previous aggressive behavior, training records, and veterinary documentation. The investigation process includes verification of policy coverage, including whether the incident falls within policy terms and exclusions.

Common Claim Denial Reasons

Insurance companies deny dog bite claims for various reasons related to policy exclusions, coverage limitations, and incident circumstances. Understanding these common denial reasons helps victims and attorneys prepare stronger claims and challenge inappropriate denials.

Several factors commonly lead to dog bite insurance claim denials:

- Breed-specific exclusions that eliminate coverage for certain dog types

- Prior bite history exclusions after previous incidents involving the same dog

- Policy lapse or non-payment issues that suspend coverage during the incident

- Intentional act exclusions when owners allegedly encouraged aggressive behavior

- Trespasser exclusions that deny coverage for injuries to uninvited visitors

Some denials result from disputes about incident circumstances, such as whether the victim was lawfully present on the property or whether the dog was provoked before biting.

Settlement Negotiation Strategies

Successful dog bite settlement negotiations require comprehensive documentation of injuries, medical treatment, and financial losses resulting from the incident. Insurance companies typically make initial settlement offers that undervalue claims, particularly for serious injuries requiring ongoing treatment.

Medical documentation becomes crucial in demonstrating injury severity and treatment necessity. Economic damages include medical expenses, lost wages, and future treatment costs that require careful calculation and documentation.

Landlord Liability for Tenant Dog Bites

Property owners who rent residential or commercial space may face liability for dog bite incidents involving tenant animals under specific legal theories. Landlord liability depends on factors such as lease terms, knowledge of dangerous dogs, and degree of control over tenant pets.

Generally, landlords do not face automatic liability for tenant dog bites simply because they own the property where incidents occur. However, certain circumstances create landlord duties and potential liability that extend beyond the tenant-dog owner relationship.

Knowledge and Control Requirements

Landlord liability for tenant dog bites typically requires proof that property owners had actual or constructive knowledge of the dog’s dangerous propensities and possessed sufficient control over the animal to prevent incidents.

Knowledge requirements may be satisfied through tenant complaints, neighbor reports, prior bite incidents, or personal observation of aggressive behavior. Control requirements examine whether landlords had authority to remove dangerous dogs or require safety measures.

Lease Agreement Pet Provisions

Lease agreements often contain pet-related provisions that affect landlord liability for dog bite incidents. These clauses may include pet deposits, breed restrictions, size limitations, and requirements for renter’s insurance coverage that includes pet liability.

Some lease agreements require tenants to carry renter’s insurance with specific liability limits for pet-related incidents. Pet screening requirements may include veterinary records, training certifications, or behavioral assessments that help landlords evaluate risks before approving tenant animals.

Common Area Incidents

Dog bite incidents occurring in common areas such as hallways, lobbies, elevators, or outdoor spaces create heightened landlord liability risks. Property owners have greater control over common areas and duties to maintain safe conditions for all residents and visitors.

Landlord liability for common area dog bites depends on whether reasonable safety measures existed and whether property owners knew about dangerous dogs using these spaces.

Comparative Fault and Damage Reductions

Both Missouri and Kansas apply comparative fault, which can reduce compensation when a victim’s conduct contributed to the incident. Missouri’s dog-bite statute expressly allows reduction for victim fault, and Kansas applies modified comparative negligence under K.S.A. 60-258a.

Provocation and Victim Conduct

Provocation represents the most common comparative fault defense in dog bite cases and examines whether victim actions triggered or contributed to aggressive behavior. Courts typically require proof that victim conduct was sufficient to cause a reasonable dog to bite.

Physical provocation may include hitting, kicking, or otherwise harming the dog before the bite incident. However, minor physical contact such as petting or attempting to move the animal typically does not constitute legal provocation.

Common comparative fault scenarios in dog bite cases include situations where victims ignore clear warning signs or engage in risky behavior:

- Approaching dogs that are eating, sleeping, or caring for puppies

- Ignoring warning signs such as growling, baring teeth, or defensive posturing

- Entering private property without permission where guard dogs are present

- Teasing, taunting, or deliberately provoking animals before bite incidents

Child victims face different comparative fault standards that consider their age, maturity, and ability to understand risks associated with dog interactions.

Trespasser Status Effects

Victim legal status at the time of dog bite incidents affects liability and comparative fault analysis. Under premises liability law, trespassers, licensees, and invitees receive different levels of protection that influence damage calculations.

Invited guests and business invitees generally receive the highest protection and face lower comparative fault risks. Missouri’s statute applies only if the person was on public property or lawfully on private property; trespassers are generally excluded. Kansas claims proceed under negligence principles, not a strict-liability statute.

Maximizing Dog Bite Insurance Recovery

Successful dog bite claims require strategic approaches that address insurance coverage issues, liability theories, and damage calculations. Experienced attorneys understand how to navigate complex insurance policies and negotiate favorable settlements for bite victims.

Multiple Insurance Sources

Dog bite incidents sometimes involve multiple insurance policies that provide coverage for different aspects of claims. Homeowner’s insurance covers dog owner liability, while renter’s insurance may provide additional coverage for tenant-owned animals.

Property owner insurance may provide coverage when landlords face liability for dangerous dogs on their premises. Umbrella insurance policies provide additional liability coverage beyond standard homeowner’s policy limits.

Documentation and Evidence Preservation

Strong dog bite claims require comprehensive documentation of incident circumstances, injuries, and financial losses. Immediate medical attention creates crucial documentation of injury severity and treatment necessity.

Photographs of bite wounds, torn clothing, and incident scenes provide objective evidence of attack circumstances and injury extent. Witness statements from people who observed the incident or the dog’s prior behavior help establish liability and refute comparative fault allegations.

FAQ for Dog Bite Liability and Insurance in Kansas City

Will homeowner’s insurance cover my dog bite claim?

Most homeowner’s insurance policies provide coverage for dog bite incidents, but coverage depends on policy terms, breed restrictions, and prior incident history. Some insurers exclude specific breeds or impose coverage limitations after previous bite claims. Insurance companies may also deny claims based on policy exclusions or disputes about incident circumstances.

Can I sue my landlord if a tenant’s dog bit me?

Landlord liability for tenant dog bites depends on whether property owners had knowledge of the dog’s dangerous propensities and sufficient control to prevent incidents. Landlords who receive complaints about aggressive dogs but fail to take action may face liability for subsequent bite incidents.

How does comparative fault affect my dog bite claim?

Missouri’s dog bite statute allows damage reduction based on victim fault, while Kansas applies modified comparative fault rules that bar recovery when victims are 50% or more at fault. Common comparative fault scenarios include provocation, ignoring warning signs, or trespassing. However, child victims receive special protection, and most dog bite situations do not involve significant victim fault.

What if the dog owner doesn’t have insurance?

Dog owners without insurance may still face personal liability for bite incidents, but collecting compensation can be challenging without insurance coverage. Some victims may have coverage through their own health insurance. Property owners or landlords may also provide alternative insurance coverage depending on incident circumstances.

How much compensation can I recover for a dog bite?

Dog bite compensation varies based on injury severity, medical expenses, lost wages, and pain and suffering damages. Serious bites that require surgery or reconstructive procedures or that cause permanent scarring may result in substantial settlements. Insurance policy limits, comparative fault reductions, and available coverage sources affect final compensation amounts.

Protecting Your Rights After Dog Bite Incidents

Dog bite incidents create complex legal and insurance challenges that require experienced legal guidance to achieve fair outcomes. Insurance companies often attempt to minimize payouts through restrictive policy interpretations, comparative fault allegations, or inadequate damage calculations.

If you or a family member suffered injuries in a dog bite incident in Missouri or Kansas, contact DM Injury Law today. We handle dog bite insurance claims throughout the Kansas City area and surrounding regions. Our experienced attorneys understand insurance coverage issues, landlord liability theories, and comparative fault defenses that affect dog bite compensation.

Call (816) 888-7500 or contact us online today for a free consultation. We’re available 24/7 and work on a contingency fee basis—you pay no attorney fees unless we win your case.

We have offices all over Missouri and Kansas, including: