After a car accident, the call from an insurance adjuster is not just a formality; it is a strategic step in a process that can determine the compensation you receive for your injuries and losses. While you are focused on healing, the adjuster is focused on investigating your claim with one primary goal: resolving it for the lowest possible cost to their company.

If an insurance adjuster called you after an accident, the clock has started on their investigation, and every word matters. Understanding the dynamics of this conversation can help safeguard your rights.

At DM Injury Law, our mission is to level the playing field between injured individuals and powerful insurance companies. This resource will provide the information you need to handle this call effectively. If you are in the Kansas City area and need immediate guidance, call (816) 888-7500 or contact us through our online form today for a free consultation.

Key Takeaways for What to Say to the Insurance Adjuster After a Car Accident

- An insurance adjuster’s primary goal is to protect their company’s financial interests by minimizing the value of a claim.

- Providing a recorded statement is generally not required and can be used to undermine a person’s injury claim later.

- Adjusters may use tactics like offering a quick, low settlement or creating a false sense of urgency to pressure claimants.

- Sharing only basic, factual information is advisable, while avoiding discussions about injuries, fault, or settlement amounts.

- Consulting with a personal injury attorney before having a detailed conversation with an adjuster can help protect a claimant’s rights.

Why Did an Insurance Adjuster Call Me After an Accident?

When an insurance adjuster calls you after an accident, it’s important to remember who they work for. Whether it’s the at-fault driver’s insurance company or your own, their job is to investigate the claim and resolve it for the lowest possible cost to their employer. They are trained negotiators whose performance is often measured by how much money they save the company.

Think of them as information-gatherers. Their goal is to get a detailed account of the accident, your injuries, and the property damage from your perspective. However, they are also listening for any information that could be used to assign you partial blame, downplay the severity of your injuries, or otherwise find reasons to reduce the value of your claim. This is why it’s critical to be careful when talking to an adjuster after an accident.

The Dangers of a Recorded Statement

One of the first things an adjuster will likely ask for is a recorded statement. They might present it as a standard, harmless step in the process, but it is a significant and potentially damaging event for your claim. You are not legally obligated to provide a recorded statement to the other driver’s insurance company, and it is often in your best interest to politely decline until you have sought legal guidance.

The reason is simple: “anything you say can be used against you.” Adjusters are skilled at asking leading questions designed to elicit answers that can be taken out of context. Even seemingly innocent phrases can be twisted to weaken your case.

Here are a few examples of common phrases and how they might be used against you:

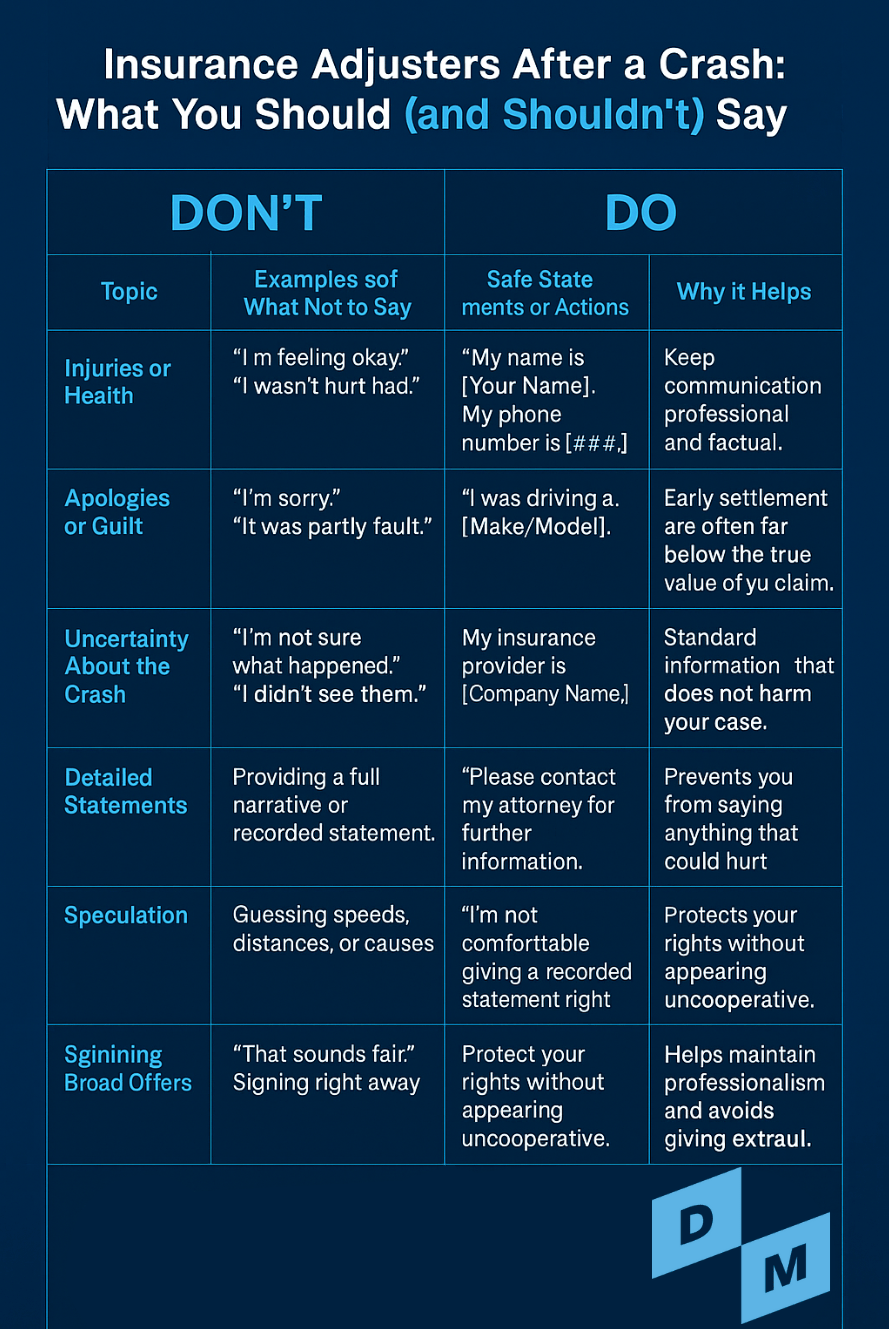

- “I’m feeling okay.”: If you say this shortly after the crash, before the full extent of your injuries is known, an adjuster may use it to argue that your injuries aren’t serious. Adrenaline can mask pain, and many injuries, like whiplash or internal damage, can take days or weeks to fully appear.

- “I’m sorry it happened.”: This is a common, polite expression of sympathy. However, an adjuster can interpret it as an admission of guilt or partial fault for the accident, even if you were just being courteous.

- “I’m not sure what happened.”: While you may still be piecing together the chaotic details of the crash, an adjuster might use this statement to suggest your memory is unreliable or that you cannot prove the other driver was at fault.

These examples highlight why a recorded statement can be a minefield for an unsuspecting accident survivor. It is always wise to consult with an attorney before agreeing to have any conversation recorded.

Common Tactics Used by Insurance Adjusters

Beyond requesting a recorded statement, adjusters employ several strategies to settle claims quickly and cheaply. Being aware of these tactics can help you recognize them and avoid making a decision that you might regret later.

- The Quick, Lowball Offer: The adjuster may offer you a settlement check within days of the accident. This can be incredibly tempting, especially when you have medical bills and car repair costs piling up. However, these initial offers are almost always far less than what your claim is actually worth. They don’t account for future medical treatment, lost wages, or the full extent of your pain and suffering. Once you accept an offer and sign a release, you cannot ask for more money later.

- Creating a False Sense of Urgency: You might hear phrases like, “This offer is only good for the next 24 hours,” or “We need to resolve this today.” This is a pressure tactic designed to make you accept a low offer before you have time to fully assess your damages or speak with a lawyer. A legitimate offer will still be there after you’ve had time to consider it.

- Requesting a Blanket Medical Authorization: The adjuster will ask you to sign a medical release form. While they do need access to records related to your accident injuries, they often send a form that gives them blanket authorization to access your entire medical history. They can then dig for pre-existing conditions or past injuries to argue that your current pain isn’t solely from the accident. You have the right to limit the authorization to only the relevant medical records.

Recognizing these strategies is the first step in protecting yourself. Remember, you control the flow of information and the timeline for making decisions about your claim.

What to Say to an Insurance Adjuster After a Car Accident

So, if you shouldn’t discuss injuries, fault, or a recorded statement, what should you say? Your goal is to be cooperative but guarded. Provide only the essential, objective facts about the incident.

Here is a list of information that is generally safe to share:

- Your full name, address, and phone number

- The date, time, and location of the accident

- The make and model of the vehicle you were driving

- The name of your own insurance company

- The name and contact information for your attorney, if you have one

You can politely state that you are not prepared to discuss the details of the accident or your injuries at this time. A simple, firm response is best: “I am still processing everything and am not ready to give a detailed statement. I can provide you with the basic information, but I will not be discussing my injuries or the accident details further today.” This shows you are not being difficult, but simply protecting your rights.

Understanding Your Rights in Missouri and Kansas

Navigating an insurance claim is even more complex because the laws that govern it can vary significantly from state to state. For residents in the Kansas City area, an accident on one side of State Line Road can be subject to completely different rules than an accident on the other.

Comparative Fault Laws

Comparative fault rules determine how compensation is handled if you are found to be partially responsible for the accident.

- Missouri: Missouri follows a rule of pure comparative negligence. Under the Missouri Revised Statutes § 537.765, you can recover damages even if you are found to be primarily at fault. However, your total compensation will be reduced by your percentage of fault. For example, if you have $100,000 in damages but are found 20% at fault, you can recover $80,000.

- Kansas: Kansas uses a modified comparative fault rule, sometimes called the 50% bar rule. According to Kansas Statutes § 60-258a, you can only recover damages if you are found to be less than 50% at fault. If you are determined to be 50% or more responsible for the crash, you are barred from recovering any compensation.

This is a critical distinction that insurance adjusters can use to their advantage if they can shift even a small amount of blame onto you.

How a Car Accident Lawyer Can Help

Dealing with an insurance adjuster after an accident can be frustrating. This is where an experienced car accident attorney can make a significant difference. When you hire a lawyer, they can immediately take over all communications with the insurance company on your behalf.

An attorney can help you by:

- Handling All Communication: Your lawyer will speak to the adjuster for you, ensuring that no damaging information is accidentally shared. This allows you to focus on your health and recovery.

- Conducting a Thorough Investigation: A legal team can gather crucial evidence, such as police reports, witness statements, and photos of the scene, to build a strong case proving the other party’s fault.

- Accurately Calculating Your Damages: They will work with you and your doctors to understand the full scope of your losses, including current and future medical bills, lost income, reduced earning capacity, and non-economic damages like pain and suffering.

- Negotiating a Fair Settlement: Armed with evidence and a full valuation of your claim, your attorney will negotiate with the insurance company from a position of strength to secure the maximum compensation you deserve.

- Filing a Lawsuit if Necessary: If the insurance company refuses to make a fair offer, your lawyer will be prepared to take your case to court to fight for your rights.

Having a knowledgeable advocate on your side levels the playing field and sends a clear message to the insurance company that you will not be pressured into an unfair settlement.

FAQs: Insurance Adjuster Called Me After Accident

Here are answers to some common questions people have after being contacted by an insurance company.

Should I talk to my own insurance company’s adjuster?

Yes, you generally have a duty to cooperate with your own insurance company under the terms of your policy. However, you should still be cautious. Stick to the facts of the accident and avoid making any statements that could be interpreted as admitting fault. It can still be beneficial to have an attorney guide you through this process.

How long does an adjuster have to respond to my claim?

The timeframes vary by state. Both Missouri and Kansas have laws that require insurance companies to act in good faith and handle claims in a timely manner. However, what is considered “timely” can be subjective. If you feel an insurer is deliberately delaying your claim, a lawyer can help enforce your rights.

What happens if I already gave a recorded statement?

If you have already given a recorded statement, it does not mean your case is lost. An experienced attorney can review the statement, understand its context, and work to mitigate any potential damage it could cause to your claim. It is important to be honest with your lawyer about what you said.

Do I have to sign the medical release form the adjuster sent me?

You should never sign any document from an insurance company without understanding exactly what it means. A broad medical release form gives them access to your entire medical history. An attorney can help you provide the insurance company with only the medical records that are relevant to your accident injuries.

Don’t Face the Insurance Company Alone

Receiving a call from an insurance adjuster can be intimidating, but you have more power than you think. By understanding their motives and knowing your rights, you can protect yourself from common pitfalls. You do not have to navigate this process by yourself.

At DM Injury Law, our team is ready to stand by your side. With a dedicated team of nearly 70 attorneys and 250 support staff members, we have the resources and experience to handle every aspect of your claim, from the initial investigation to the final settlement. We work on a contingency fee basis, which means you pay nothing unless we recover compensation for you.

Contact us today for a free, no-obligation consultation to discuss your case. Call our Kansas City office at (816) 888-7500 or fill out our online form to get started.

Past results do not guarantee future outcomes. Every case is different and must be evaluated on its own facts.