After an accident, finding out the driver who hit you doesn’t have car insurance adds a layer of profound frustration and uncertainty to an already traumatic event. Suddenly, you’re not just dealing with injuries and a damaged vehicle; you’re wondering, “Who is going to pay for all of this?” — something a Kansas City car accident lawyer can help you navigate.

If this has happened to you, you are not out of options. In Kansas, you have a specific path to recovery. An uninsured motorist claim in Kansas can help you get the compensation you need to move forward.

At DM Injury Law, our team of dedicated attorneys and staff understands the stress an accident with an uninsured driver can cause. We are here to help you understand your rights and fight for the compensation you deserve after a crash. Call (316) 888-7500 or contact us through our online form today for a free consultation.

Call (816) 888-7500 or contact us online today for a free consultation.

Key Takeaways for Uninsured Motorist Claim in Kansas

- Kansas state law requires all auto insurance policies to include Uninsured/Underinsured Motorist (UM/UIM) coverage.

- An uninsured motorist claim is filed with the injured person’s own insurance company, not the at-fault driver’s.

- This essential coverage can help pay for medical expenses, lost income, and damages for pain and suffering.

- Even though it is a claim with one’s own insurer, the process can become adversarial as the company may try to minimize its payout.

- Strict legal deadlines, known as statutes of limitations, apply to personal injury and uninsured motorist claims in Kansas.

What Is an Uninsured Motorist Claim in Kansas?

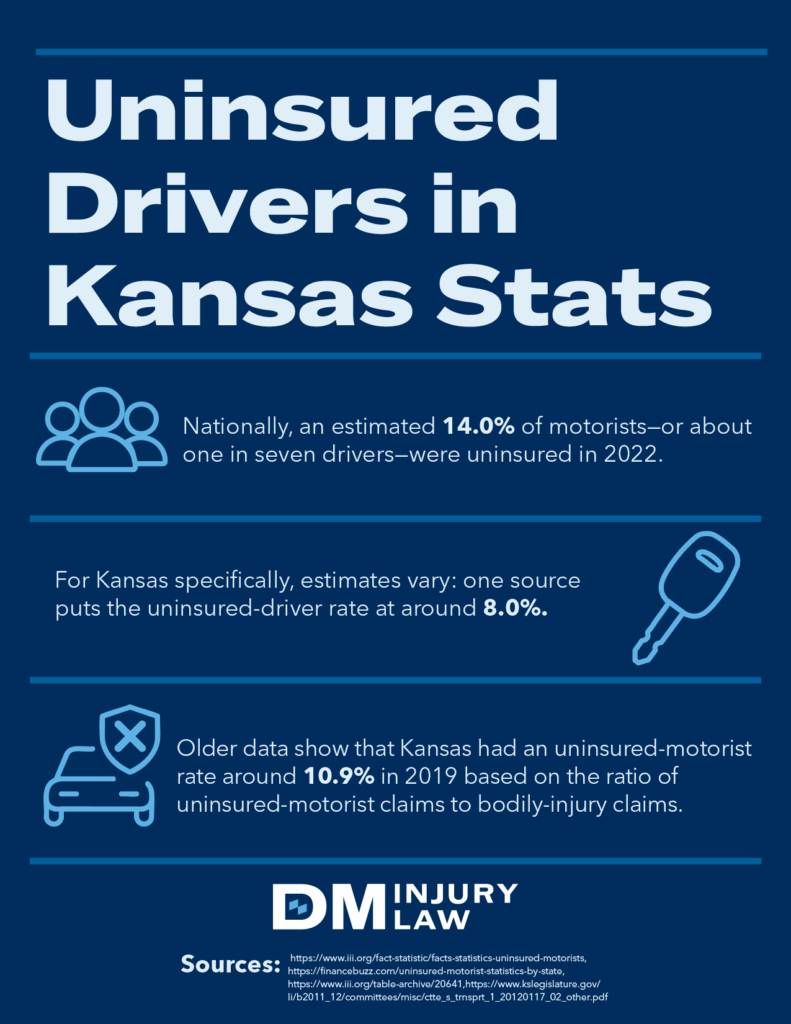

An uninsured motorist claim is a type of insurance claim you file with your own auto insurance provider after you have been injured in an accident caused by a driver who has no liability insurance. It’s a frustrating reality that, despite state laws, many drivers are on the road illegally without coverage. In fact, the Insurance Research Council estimates that more than one in seven drivers nationwide is uninsured. Kansas is no exception, with 12.5% of drivers being uninsured.

Normally, after a car accident, you would file a claim against the at-fault driver’s liability insurance. But when there is no insurance to claim against, your Uninsured Motorist (UM) coverage kicks in. Your own insurance company essentially “steps into the shoes” of the at-fault driver’s insurer and becomes responsible for paying for your damages up to your policy limits.

While this may sound straightforward, it creates a unique and often difficult situation. Your insurance company, which you pay for protection, now has a financial interest in paying you as little as possible. This is why an uninsured motorist claim can quickly become just as complex and contentious as dealing with an opposing insurance company — especially when you must sue after a car accident.

Understanding Kansas UM/UIM Coverage Requirements

The good news for drivers in the Sunflower State is that this protection is mandatory. Kansas law requires insurance companies to include both Uninsured Motorist (UM) and Underinsured Motorist (UIM) coverage in every auto policy sold in the state, unless it is specifically rejected in writing.

According to Kansas Statutes § 40-284, the minimum coverage limits you must carry are:

- $25,000 in bodily injury liability coverage per person

- $50,000 in bodily injury liability coverage per accident

It is important to understand the difference between these two crucial types of coverage:

- Uninsured Motorist (UM) Coverage: This applies when the at-fault driver has no insurance at all, or when you are the victim of a hit-and-run and the driver cannot be identified.

- Underinsured Motorist (UIM) Coverage: This applies when the at-fault driver has insurance, but their policy’s bodily injury limits are too low to cover the full extent of your damages.

While these are the minimums, it is always a good idea to purchase higher UM/UIM limits if you can afford to. The costs of a serious accident can easily exceed these minimum amounts, and having extra coverage provides a vital safety net for you and your family — especially when common car defects play a role in causing or worsening a crash.

What Can an Uninsured Motorist Claim in Kansas Cover?

Your UM coverage is designed to compensate you for the same types of losses that the at-fault driver’s insurance would have covered if they had it. It is focused on “bodily injury,” which is a legal term for the physical and financial harm you suffer.

- Medical Expenses: This includes all costs associated with your medical care resulting from the crash. It covers everything from the initial ambulance ride and emergency room visit to surgeries, hospital stays, physical therapy, prescription medications, and any anticipated future medical care.

- Lost Wages and Earning Capacity: If your injuries prevent you from working, your UM claim can reimburse you for the income you have lost. Furthermore, if the injuries are severe enough to cause a long-term or permanent disability that affects your ability to earn a living in the future, you can seek compensation for this “loss of earning capacity.”

- Pain and Suffering: This is compensation for the non-economic harm you have endured. It acknowledges the physical pain, emotional distress, anxiety, and trauma caused by the accident and your injuries. Calculating this value is complex, as it is subjective, but it is a critical part of your recovery.

- Other Damages: Depending on the severity of your injuries, you may also be entitled to compensation for things like permanent scarring or disfigurement, loss of a limb, or the inability to enjoy hobbies and activities you once loved (known as “loss of enjoyment of life”).

Pursuing all these avenues of compensation ensures that your final settlement or award reflects the true and total impact the accident has had on your life, no matter who ultimately caused the car accident.

Navigating Challenges with Your Own Insurance Company

A common and dangerous mistake people make is assuming their own insurance company will treat them fairly simply because they are a loyal, paying customer. In an uninsured motorist claim, your insurer’s role changes. They are no longer just your protector; they are the party responsible for paying the claim, which puts them in a direct financial conflict with you. Their goal is to protect their bottom line by minimizing the payout — a reality that often becomes clear when you go to court for a car accident.

Be aware of these common tactics used to devalue or deny claims:

- Offering a quick, lowball settlement before you know the full extent of your injuries.

- Claiming your injuries were caused by a pre-existing condition.

- Disputing the reasonableness or necessity of your medical treatments.

- Using recorded statements to twist your words and assign partial fault to you.

- Delaying the process in the hope that you will become frustrated and accept less than you deserve.

Facing these tactics alone can be overwhelming, especially when you are trying to recover from your injuries. This is where having an experienced advocate on your side becomes invaluable.

The Statute of Limitations for Your Claim

In the legal world, a “statute of limitations” is a strict deadline for filing a lawsuit. If you miss this deadline, you lose your right to seek compensation in court forever, no matter how strong your case is.

In Kansas, the statute of limitations for most personal injury claims is two years from the date of the accident, as outlined in Kansas Statutes § 60-513. However, an uninsured motorist claim Kansas can be more complicated. Your insurance policy is a contract, and it may contain different deadlines or requirements for filing a claim or a lawsuit against the insurance company itself.

These contractual deadlines can sometimes be even shorter than the two-year state limit. It is absolutely critical to understand these timelines. Waiting too long can jeopardize your entire case. Consulting with an attorney as soon as possible after your accident ensures that all deadlines are identified and met — especially when you’re also worried about how long a car accident stay on your record and how that might affect your future.

Call (816) 888-7500 or contact us online today for a free consultation.

How a Personal Injury Attorney Can Make a Difference

Trying to handle a Kansas uninsured motorist claim on your own puts you at a significant disadvantage. The insurance adjuster you are dealing with handles these claims every day. They are trained negotiators whose job is to save the company money. A dedicated personal injury attorney levels the playing field and manages every aspect of your claim so you can focus on healing — especially if you’re worried about what happens when someone is driving my car and gets in an accident and how that could affect your insurance and liability.

- Thoroughly Investigating the Accident: An attorney will secure the police report, interview witnesses, and gather all evidence needed to definitively prove the other driver was at fault and uninsured.

- Calculating the Full Value of Your Claim: This goes far beyond just adding up your current medical bills. A legal team can work with medical experts and financial planners to project your future medical needs and lost income to ensure your settlement covers your long-term recovery.

- Handling All Insurance Company Communications: Your attorney becomes the single point of contact for the insurance company. This protects you from saying something that could be used against you and stops the adjusters from harassing you with requests and low offers.

- Skillfully Negotiating a Fair Settlement: Experienced attorneys know the tactics insurers use and how to counter them. They leverage the evidence and their understanding of Kansas law to negotiate for the maximum compensation possible.

- Taking Your Case to Court If Necessary: While most cases settle out of court, your attorney’s willingness and ability to file a lawsuit and fight for you at trial gives you powerful leverage. Insurance companies are far more likely to offer a fair settlement when they know you have a proven trial lawyer ready to go to court.

Having a strong legal advocate transforms the process from an uphill battle into a fair fight for the justice you deserve.

FAQs: Uninsured Motorist Claim Kansas

Here are answers to some common questions we hear from people dealing with a crash with an uninsured driver.

What if the uninsured driver fled the scene after the accident?

If you were the victim of a hit-and-run, your Uninsured Motorist (UM) coverage should still apply. It is crucial that you report the accident to the police immediately and notify your insurance company as soon as possible. In Kansas, there generally must be evidence of physical contact between your vehicle and the phantom vehicle for your UM coverage to be triggered.

What is the difference between UM/UIM and PIP coverage in Kansas?

Personal Injury Protection (PIP) is Kansas’s no-fault coverage that is the first payer for your initial medical bills and lost wages, regardless of who caused the accident. UM/UIM coverage is fault-based and applies only when an uninsured or underinsured driver caused your injuries. It is designed to cover damages that exceed your PIP limits.

Do I have to pay a lawyer up front to handle my uninsured motorist claim?

No. Reputable personal injury law firms, including ours, operate on a contingency fee basis. This means we only collect a legal fee if we successfully recover money for you through a settlement or verdict. There are no upfront costs, and if we don’t win your case, you owe us nothing.

A Dedicated Kansas Legal Team Can Help with Your Uninsured Motorist Claim

Being hit by an uninsured driver can leave you feeling helpless and alone. But you have rights, and you have options. The experienced team at DM Injury Law, with approximately 70 attorneys and 250 support staff members, has the resources, knowledge, and dedication to guide you through every step of your uninsured motorist claim. We are committed to holding insurance companies accountable and fighting for the full and fair compensation our clients need to rebuild their lives.

Because we work on a contingency fee basis, there is no financial risk to you. If we don’t win, you don’t pay. Don’t let an insurance company decide your future. Contact DM Injury Law today for a free, no-obligation consultation to discuss your case. Call our Wichita office at (316) 888-7500 or our Topeka office at (785) 444-4444, or fill out our online form to get started.

Past results do not guarantee future outcomes. Every case is different and must be evaluated on its own facts.

Call (816) 888-7500 or contact us online today for a free consultation.