For many families, a dog is more than a pet; it is a beloved member of the family. The bond we share with our dogs is a source of joy and comfort. But when a dog bite incident occurs, it can create a situation filled with stress, confusion, and fear.

This distress is often magnified when victims and dog owners alike discover that their homeowners’ insurance policy, which they trusted to protect them, refuses to cover the incident. This is a common and heartbreaking reality for owners of certain breeds due to a homeowners insurance pit bull exclusion or similar clauses targeting other dogs, something a Kansas City dog bite lawyer regularly helps families navigate.

At DM Injury Law, we understand how stressful dog bites can be, whether you are the injured party or the dog’s owner facing a devastating financial and personal crisis. Our team is here to provide clarity and guidance through these complex legal and insurance challenges. Call (816) 888-7500 or contact us online today for a free consultation.

Call (816) 888-7500 or contact us online today for a free consultation.

Key Takeaways for Homeowners Insurance Pit Bull Exclusion

- Many standard homeowners insurance policies include specific clauses that exclude liability coverage for bites from certain dog breeds.

- Breeds commonly found on exclusion lists include Pit Bulls, Rottweilers, German Shepherds, Dobermans, and others perceived as high-risk.

- A coverage denial due to a breed exclusion can leave the dog owner personally responsible for all damages, including medical bills and lost wages.

- Dog bite liability laws differ significantly between states like Missouri, Kansas, Oklahoma, and Colorado, impacting how a claim is handled.

- Homeowners may have options, such as purchasing separate canine liability insurance, to ensure they are protected.

Why Do Insurance Companies Exclude Certain Dog Breeds?

When a person is injured by a dog, the owner’s homeowners or renters insurance is typically the first place they turn to for compensation. This is because liability coverage—the part of the policy that pays for injuries to others—is designed for these situations. However, many insurance providers have created lists of dog breeds they will not cover, which can complicate dog bite liability and insurance coverage.

Insurance companies operate on a model of risk assessment. They analyze data to predict the likelihood of having to pay out a claim. Based on certain statistics, which are often debated and criticized for being incomplete, some breeds have been labeled “high-risk” or “dangerous.”

Insurers argue that these breeds are involved in a disproportionate number of bite incidents, leading to more frequent and expensive claims. To minimize their financial risk, they simply refuse to cover these dogs.

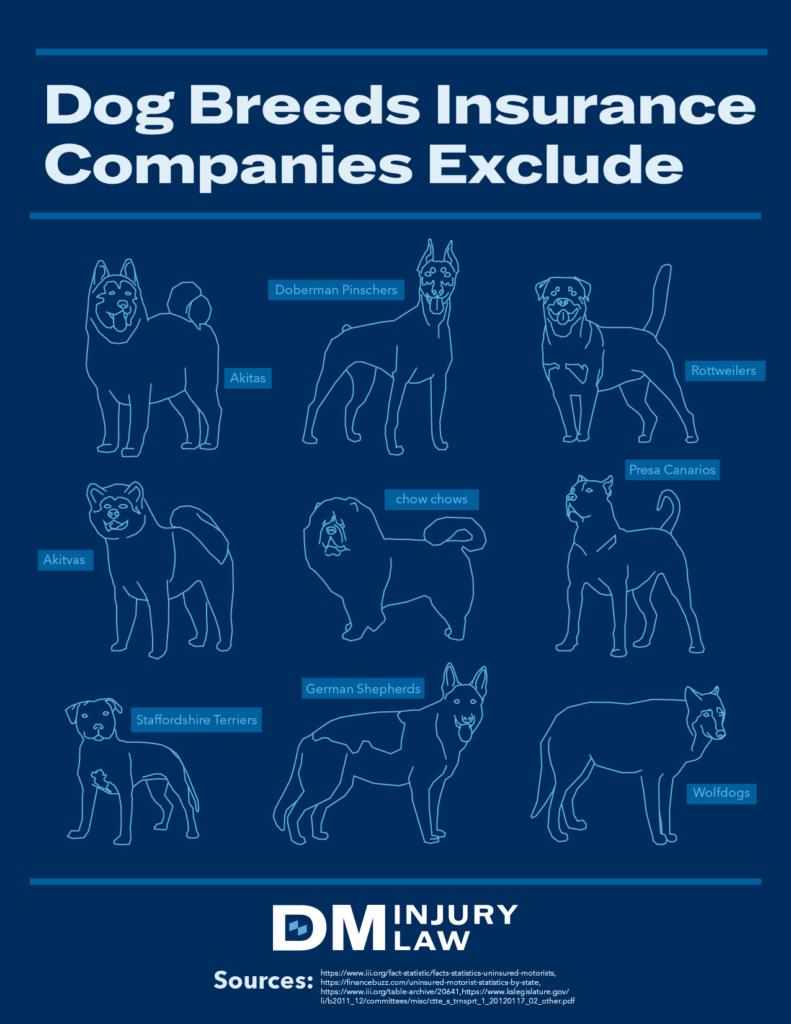

This practice, known as having a breed exclusion list, affects countless responsible dog owners. Some of the breeds most frequently excluded from policies include:

- Pit Bull Terriers

- Staffordshire Terriers

- Rottweilers

- Doberman Pinschers

- German Shepherds

- Chow Chows

- Presa Canarios

- Akitas

- Wolf-hybrids

This list is not exhaustive, and the specific breeds an insurer might exclude can vary from one company to another. The existence of these lists means that a loving family pet could become a major financial liability, even if the dog has never shown a hint of aggression.

Your Homeowners Insurance Policy and a Pit Bull Exclusion

It’s a shock for many to learn that their loyal companion could void a crucial part of their insurance coverage. A breed exclusion is a specific clause written into an insurance policy that states the company will not pay for any damages or injuries caused by a specific breed of dog owned by the policyholder. A pit bull insurance denial is one of the most common examples of this practice in action, raising urgent questions about what to do after a dog bite.

When an insurance company denies a claim based on this exclusion, the financial responsibility falls squarely on the dog owner’s shoulders. This means they could be personally sued for the victim’s:

- Medical Expenses: Including emergency room visits, surgery, physical therapy, and psychological counseling.

- Lost Wages: Compensation for the time the injured person was unable to work while recovering.

- Pain and Suffering: Damages for the physical pain and emotional trauma caused by the attack.

These costs can easily climb into the tens or even hundreds of thousands of dollars, a burden most families cannot afford. To avoid a devastating surprise, it is vital to know exactly what your policy says.

- Read the “Exclusions” Section in Your Policy: This is where you will find specific language about what is not covered. Look for any mention of animals, dogs, or specific breed names.

- Ask Your Agent Direct Questions: Do not rely on assumptions. Call or email your insurance agent and ask directly, “Does my policy have any dog breed exclusions?” It is always best to get their answer in writing.

- Disclose Your Pets: When you get a new dog, inform your insurance company. While this might lead to a higher premium or the need to find a new insurer, it is far better than having a future claim denied because you weren’t transparent.

Taking these steps can help you understand your coverage and protect your family from a potential financial catastrophe.

How Dog Bite Laws Vary in the Midwest

The situation becomes even more complicated because the laws governing a dog owner’s responsibility change from state to state. Here is a brief overview of the laws in Missouri, Kansas, Oklahoma, and Colorado.

Missouri’s Strict Liability Law

Missouri follows a “strict liability” statute for dog bites. This means a dog owner is automatically responsible for the injuries their dog causes, regardless of whether the dog had ever been aggressive before.

The victim does not need to prove that the owner was negligent or knew the dog was dangerous. For the owner to be held liable, the injured person must have been on public property or lawfully on private property and must not have provoked the dog.

Kansas and the “One-Bite Rule”

Kansas generally adheres to a “one-bite rule,” which is based on common law rather than a specific statute. Under this rule, an owner is typically only held liable if they knew or should have known that their dog had a tendency to be dangerous. This could be because the dog had bitten someone before or had shown other aggressive behaviors.

However, an owner can also be held responsible if they were negligent—for example, by violating a local leash law—and that negligence led to the injury.

Oklahoma’s Strict Liability Law

Similar to Missouri, Oklahoma has a strict liability dog bite statute (OK Stat § 4-42.1). An owner is liable for the full amount of damages caused by their dog, even if they had no prior knowledge of the dog’s potential to bite. The law applies as long as the victim was lawfully on the property and did not provoke the animal. This puts a significant legal burden on dog owners in the state.

Colorado’s Approach

Colorado law also uses a strict liability standard, but it is specifically for “serious bodily injury” or death. Serious bodily injury involves a substantial risk of death, permanent disfigurement, or long-term impairment. For less severe injuries, the injured person may need to prove the owner was negligent to recover compensation.

These differing state laws create a complex legal landscape. When a homeowner’s insurance dangerous breed exclusion is also in play, a dog bite case can become incredibly difficult to navigate without experienced legal guidance.

Nebraska’s Laws

Dog bite laws in Nebraska impose strict liability on dog owners for injuries caused by their dogs, regardless of the owner’s knowledge of the dog’s dangerous propensities. However, there are specific exceptions and additional requirements for dangerous dogs, as well as distinctions in liability for landlords and other individuals who may have control over a dog.

Call (816) 888-7500 or contact us online today for a free consultation.

What Are Your Options After a Homeowners Insurance Denial?

Receiving a denial letter from your insurance company can feel like a final, devastating blow. However, it is important to remember that you may still have options, whether you are the dog owner or the injured party, and to understand how long it may take to settle a dog bite claim.

For the Dog Owner:

- Carefully Review the Denial: The denial letter must state the specific reason for the decision. Make sure you understand exactly why the claim was denied.

- Check for Factual Errors: Was your dog’s breed misidentified? Sometimes, mixed-breed dogs are incorrectly labeled. If you have documentation from a veterinarian about your dog’s actual breed, it could be grounds for an appeal.

- Explore the Appeals Process: You have the right to appeal the insurance company’s decision. This is a formal process where you can present evidence to argue that the claim should be covered. However, coverage denial appeals can be complex and challenging to win without assistance.

- Seek Alternative Coverage: Proactively, look for insurance companies that do not have breed restrictions or purchase a separate canine liability policy. These policies are specifically designed to cover injuries caused by your dog.

For the Bite Victim:

Even if the owner’s insurance company denies the claim, the owner is still legally responsible for the harm their dog caused. This means you may need to file a personal injury claim directly against the dog owner. This can be an emotionally difficult path, especially if the owner is a neighbor, friend, or family member.

It is crucial to understand that seeking compensation is not about punishing the owner; it is about ensuring you have the financial resources you need to heal and recover. A successful personal injury claim can help you cover your medical bills and lost income so that a single moment does not derail your life.

How a Personal Injury Attorney Can Help

Whether you are dealing with a bite from a neighbor’s dog in a quiet Denver suburb or an incident at a park in Tulsa, the legal details are complex. An insurance exclusion adds another layer of difficulty, making it feel like the system is working against you. This is where a dedicated personal injury attorney can make a significant difference, particularly when determining your dog bite injury settlement amount.

An experienced legal team can help by:

- Investigating the Incident: They will gather all the necessary evidence, including police reports, medical records, witness statements, and any history of the dog’s behavior.

- Analyzing the Insurance Policy: Attorneys can scrutinize the insurance policy and the denial letter to identify any weaknesses in the company’s reasoning or potential grounds for an appeal.

- Identifying All Sources of Compensation: They will explore every possible avenue for recovery, which may include other insurance policies or the personal assets of the responsible party.

- Handling All Negotiations: A lawyer will communicate directly with the insurance company or the dog owner’s legal team on your behalf, protecting you from pressure and fighting for a fair settlement.

- Filing a Lawsuit if Necessary: If a fair settlement cannot be reached, your attorney will be prepared to take your case to court to hold the responsible party accountable.

Having a knowledgeable advocate on your side can provide peace of mind and ensure your rights are protected every step of the way.

FAQs: Homeowners Insurance Breed Exclusions

Here are answers to some common questions we receive about dog bite claims and insurance coverage.

What if my dog is a mixed breed that looks like a pit bull?

This is a common issue. An insurance company may deny a claim based on its perception of the dog’s breed. In these cases, documentation from a veterinarian or even a DNA test may be used to challenge the insurer’s classification during an appeal.

Can an insurance company cancel my policy if I get a pit bull?

Yes, an insurance company can choose not to renew your policy or cancel it (with proper notice) if you acquire a dog from their restricted breed list. This is why it is so important to communicate with your insurer before bringing a new pet home.

Are there insurance companies that do not have breed restrictions?

Yes, some insurance companies have moved away from breed-specific exclusions. Instead, they evaluate dogs on an individual basis, looking at factors like bite history and training. It may require some research to find these providers, but they do exist.

Does a “Beware of Dog” sign help or hurt my case as an owner?

It can be complicated. While the sign shows you took a step to warn others, a court or insurance company could interpret it as evidence that you already knew your dog was potentially dangerous. This could actually work against you, particularly in a state with a “one-bite rule.”

What if the bite happened at a public park and not on the owner’s property?

A homeowner’s insurance policy’s liability coverage typically extends to incidents that happen off the owner’s property. Therefore, if coverage is not excluded for another reason (like breed), the policy should still apply even if the bite occurred at a park, on a sidewalk, or in another public place.

Contact DM Injury Law for a Free Consultation

A dog bite is incredibly stressful, and a denied insurance claim can make you feel hopeless. At DM Injury Law, our dedicated team of attorneys has the experience and resources to handle these complex cases. We are committed to helping victims fight for the full compensation they deserve and guiding dog owners through this difficult process. We believe in holding the right parties accountable and ensuring you have the support you need to move forward.

If you or a loved one has been affected by a dog bite and is facing an insurance denial, don’t wait to seek help. Contact us today at (816) 888-7500 or through our online form for your free case consultation.

Past results do not guarantee future outcomes. Every case is different and must be evaluated on its own facts.

Call (816) 888-7500 or contact us online today for a free consultation.